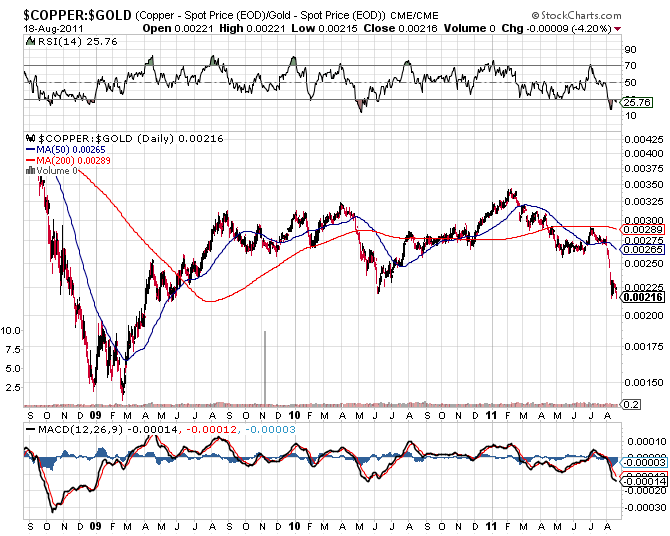

I like making random gold ratio charts in stockcharts.com since it lets you chart the ratio of anything: gold:oil, gold:copper, gold:SPX, etc:

-

If you do this kind of analysis on a longer-term basis, you see that gold is getting a bit expensive relative to other commodities, capital goods or labor (or you could say that each of those things is getting cheap when priced in gold). What is clear is that gold is no longer cheap by any measure. I don’t think this type of analysis has anything to do with where gold price goes in the near-term (technicals and sentiment drive that), but it’s helpful to think about where gold is on an historical basis.

- The Gold:Oil and Gold:Copper ratios are moderately high, and would be off the charts if oil and copper were to crash.

- Rent on a nicer 1BR apartment in Manhattan has fallen from 8 ounces in 2001 to 2 ounces today. This is about what it cost in the 1920s-60s.

- 10 ounces in 2001 bought a 12-year-old Honda Civic, and now it gets you a brand new one with extras. A Model T Ford cost 15 ounces by the 1920s. The VW Beetle cost 30-50 ounces in the ’50s.

- Median family income in was about 50 ounces in 1920, 90 ounces in 1955, over 100 in 1965, 70 in 1975, 75 in 1985, 95 in 1995 and way over 100 in 2000. Today, it’s about 30.

On a purchasing power basis, gold is adequately priced – it is certainly no longer cheap. Of course, markets don’t care about this on anything but the longest term – gold was overvalued at $500 in 1979, but it still spiked over $800 and then fell to a ridiculously low level in 2000. In the scenario where the dollar goes to zero, everything will soar in dollars, not just gold, so you’d still have to evaluate gold in terms of goods and services.

I’m still in the dollar bull camp for the foreseable future. Treasuries are pointing the way (record low 10-year yields, 3.5% on the 30-year, almost like Japan), and it looks like another bout of deflation is underway, if you define deflation as a contraction in money and credit (if credit is marked to market). Europe’s soveriegn debt implosion is deflationary. The same goes for the Australian real estate collapse and the pending RE collapses in China and Canada, and the US muni and junk market troubles.

I don’t see the dollar as any worse fundamentally than the euro or yen, and much better technically. Japan’s history since ’89 is proof that printing and spending and running up huge public debt doesn’t necessarily kill your currency. When there is too much private debt going bad but not being written off, it overwhelms the mismanagement of the currency and props it up. It doesn’t matter what you think of the fundamental value of the dollar if you’re in debt and can’t find enough dollars to make your payments. And until asset and labor prices and demand for goods and services can justify borrowing costs, there’s no credit expansion so no inflation.

Sentiment-wise, we’ve still got a great long-term case on the long-dollar trade. Fear of the dollar has been widespread since early 2008, but the DXY has just bounced around sideways – no crash. The crash happend from 2000-08, while nobody but old-school Austrians noticed.

It seems that we have settled into wave Primary 3 down, this time for real. The world is continuing to trust US treasuries, as you noted here and previously, and the dollar’s impending rise should, I would think, temper some of the comparisons of this country with Greece. It’s strange though, because we are like Greece, but for the time being it seems that we will look like a safe haven even as the broader US economy continues to decline in terms of employment, real estate, etc.

Well, we are like Greece in that default is inevitable, but the timing makes all the difference. We can make our debt payments for many more years, whereas the Greeks are already unable and will have to outright default within a year or two.

I agree that we’re probably in bear market #3 since the big top in 2000. The whole secular bear should drag on for 5 years or longer, until we finally get back to real value. The dollar will be fine for the time being – it’s gold I’m worried about.

Hi Mike,

I was wondering if you might be willing to shed some light on this.

I was watching SPY puts today, and noticing that some were not moving despite a 31 point drop (so far) in the S&P.

Some Dec 2012, Jun 2012, and Dec 2013 SPY puts, that were recently quite sensitive to movements in the S&P showed no change at all.

How can volume on the same puts that were recently sensitive have a zero volume on a day like today when the market is showing a significant drop?

Hi Bjorn,

Take another look. The bids have changed – it’s just that volume is low on this Friday before Labor Day, so not a lot of options have traded at the new prices. Also, the VIX hasn’t moved much – traders just aren’t panicking. No new lows here – just a down move in what’s been a sideways market for the last two weeks.

-Mike

BTW, if you are looking for high put prices, those are generally found after a succession of big down days. The same puts will always be cheaper after the market digests the move.

Thanks Mike, that’s very helpful

Hi Mike,

I was wondering what you think of the coming Fed QE and White House job policy. From what little I have read, it appears that this Operational Twist will not be beneficial. Also I was curious what your thoughts are of real estate thank so much.

Bobby

Please, anyone – what is the historical Gold/Wheat ratio?

Never mind – found it here:

http://www.mcoscillator.com/learning_center/weekly_chart/the_gold_wheat_ratio/

I wanted to look at wheat, since demand is less elastic (isn’t it?), and its utility per bushel is more or less unchanged with time. Looks like gold is high relative to wheat, as well.